Can You Buy a House After Bankruptcy? Your Complete Guide to Homeownership Recovery

Discover how to buy a home after bankruptcy in New Jersey. Learn about waiting periods, loan options, credit rebuilding strategies, and steps to mortgage approval after Chapter 7 or Chapter 13 bankruptcy.

Bankruptcy doesn't have to be the end of your homeownership dreams. While a Chapter 7 bankruptcy can remain on your credit report for up to ten years and Chapter 13 for about seven years, thousands of New Jersey residents successfully purchase homes after bankruptcy every year by understanding waiting periods, choosing the right mortgage product, and rebuilding their credit strategically.

If you've experienced bankruptcy, you're not alone. According to recent data, New Jersey sees thousands of bankruptcy filings annually, and many of these individuals go on to become successful homeowners. The key is understanding the process, being patient during required waiting periods, and taking deliberate steps to rebuild your financial foundation.

Can You Actually Buy a House After Bankruptcy?

The short answer is yes. Buying a house after bankruptcy is absolutely possible, though the exact path depends on several factors including the type of bankruptcy you filed, how much time has passed, and which mortgage program you're pursuing. The mortgage industry recognizes that bankruptcy is sometimes a necessary financial tool, and lenders have established clear guidelines for when and how you can qualify for a home loan after bankruptcy.

The process requires patience, strategic planning, and often professional guidance from a mortgage expert familiar with post-bankruptcy lending. In New Jersey's competitive housing market, understanding these requirements early can help you set realistic timelines and avoid disappointment.

Understanding Bankruptcy Types and Their Impact

Before diving into mortgage options, it's important to understand how different bankruptcy types affect your homebuying timeline. The two most common forms of personal bankruptcy are Chapter 7 and Chapter 13, and they have different implications for mortgage eligibility.

Chapter 7 Bankruptcy: Liquidation

Chapter 7 bankruptcy, often called "liquidation bankruptcy," eliminates most unsecured debts like credit cards and medical bills. This type of bankruptcy stays on your credit report for up to ten years, though its impact on your credit score diminishes over time. For mortgage purposes, lenders focus on the discharge date—when the court officially eliminates your debts—rather than the filing date.

Chapter 13 Bankruptcy: Reorganization

Chapter 13 bankruptcy involves a court-approved repayment plan where you pay back a portion of your debts over three to five years. This type remains on your credit report for approximately seven years. Interestingly, Chapter 13 often allows for shorter waiting periods before mortgage eligibility because it demonstrates your commitment to repaying debts rather than simply discharging them.

Discharge vs. Dismissal: A Critical Distinction

Understanding the difference between discharge and dismissal is crucial for your mortgage timeline. A discharge means the court has eliminated your debt and you no longer owe creditors. A dismissal means the court closed your case but your debt remains. Lenders view these very differently, with dismissals typically requiring longer waiting periods.

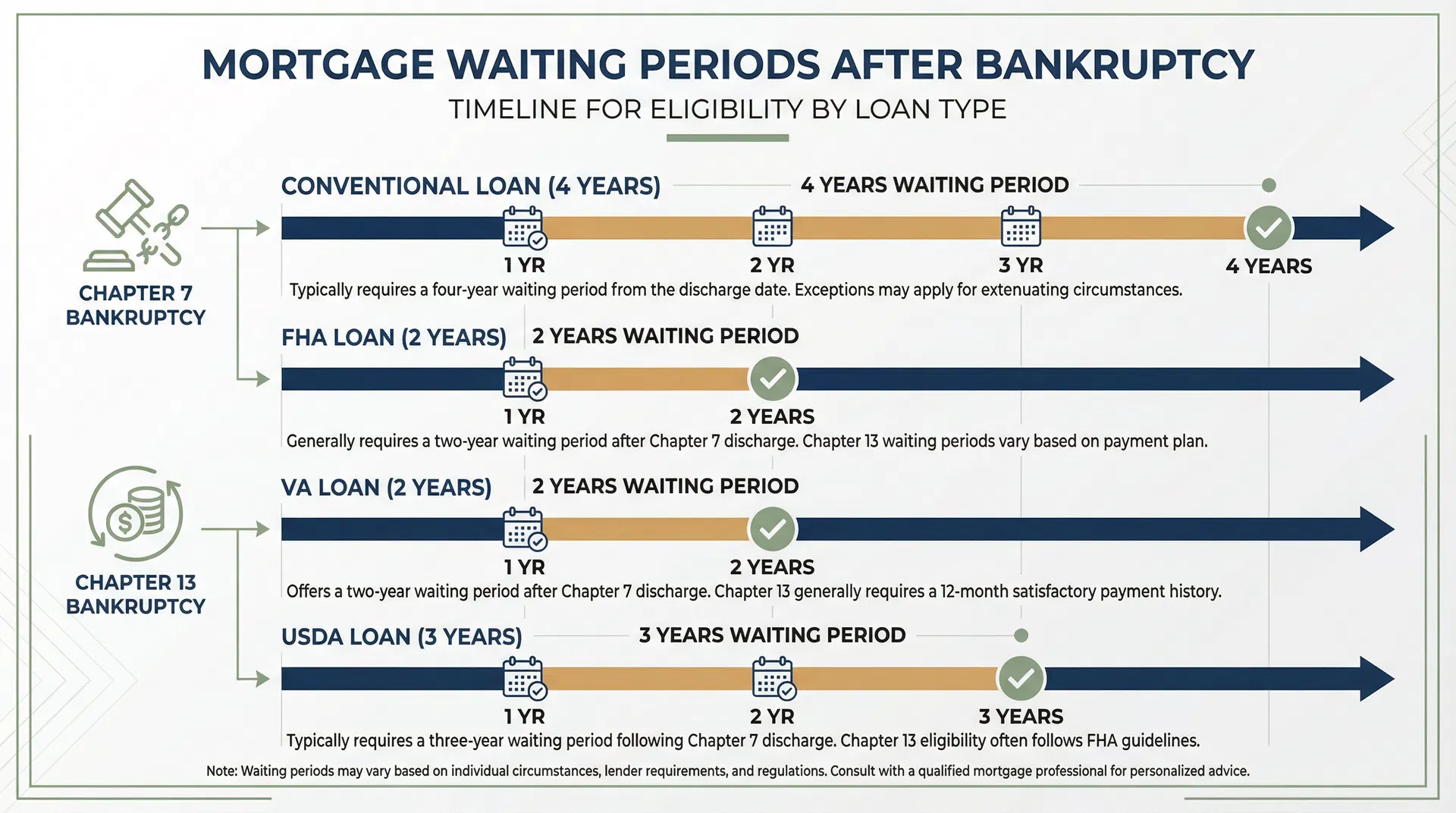

Mortgage Waiting Periods After Bankruptcy

One of the most important factors in buying a home after bankruptcy is the "seasoning period"—the required waiting time between your bankruptcy discharge or dismissal and your mortgage application. These waiting periods vary significantly based on the loan type and bankruptcy chapter.

| Loan Program | Chapter 7 Waiting Period | Chapter 13 Waiting Period |

|---|---|---|

| Conventional | 4 years (2 years with extenuating circumstances) | 2 years from discharge / 4 years from dismissal |

| FHA | 2 years (12 months with documented extenuating circumstances) | 12 months with satisfactory payment history |

| VA | 2 years from discharge | 12 months of satisfactory payments |

| USDA | 3 years from discharge | 12 months (follows FHA guidelines) |

What Are Extenuating Circumstances?

Extenuating circumstances are unusual or rare events that can explain negative items on your credit report and potentially reduce waiting periods. Examples include significant medical emergencies, extended unemployment due to economic conditions beyond your control, or death of a primary wage earner. To qualify for reduced waiting periods, you must demonstrate that these circumstances were beyond your control and are unlikely to recur.

Mortgage Options After Bankruptcy

Nothing permanently excludes you from any specific loan type after bankruptcy. However, each mortgage program has different requirements, and some are more accessible than others depending on your situation. Understanding these options helps you choose the best path forward.

Conventional Loans

Conventional loans are issued by private lenders and not backed by the federal government. While they typically require longer waiting periods after bankruptcy, they can offer competitive rates and terms once you qualify.

Conventional Loan Requirements:

- Credit Score: No official minimum, but most lenders require 620+

- Down Payment: 3% for fixed-rate, 5% for ARM

- PMI: Required if down payment is less than 20%

- Best For: Borrowers with strong credit recovery and larger down payments

FHA Loans

FHA loans are insured by the Federal Housing Administration and designed to be more accessible, especially for first-time homebuyers and those with credit challenges. These loans are often the fastest path to homeownership after bankruptcy.

FHA Loan Requirements:

- Credit Score: 580 minimum (500-579 with 10% down)

- Down Payment: 3.5% with 580+ score, 10% with 500-579

- Mortgage Insurance: Required for life of loan with less than 10% down

- Best For: First-time buyers and those with limited down payment funds

VA Loans

VA loans are available to active-duty military personnel, veterans, and eligible surviving spouses. These loans offer some of the most favorable terms available, including no down payment requirement and competitive interest rates.

VA Loan Requirements:

- Credit Score: No VA minimum (lenders typically require 620+)

- Down Payment: None required

- Mortgage Insurance: None (funding fee applies)

- Best For: Eligible veterans and service members

USDA Loans

USDA loans help low- to moderate-income borrowers purchase homes in eligible rural and suburban areas. In New Jersey, many areas outside major cities qualify for USDA financing.

USDA Loan Requirements:

- Credit Score: 640 minimum for most lenders

- Down Payment: None required

- Income Limits: Must meet area median income requirements

- Best For: Rural/suburban buyers with moderate income

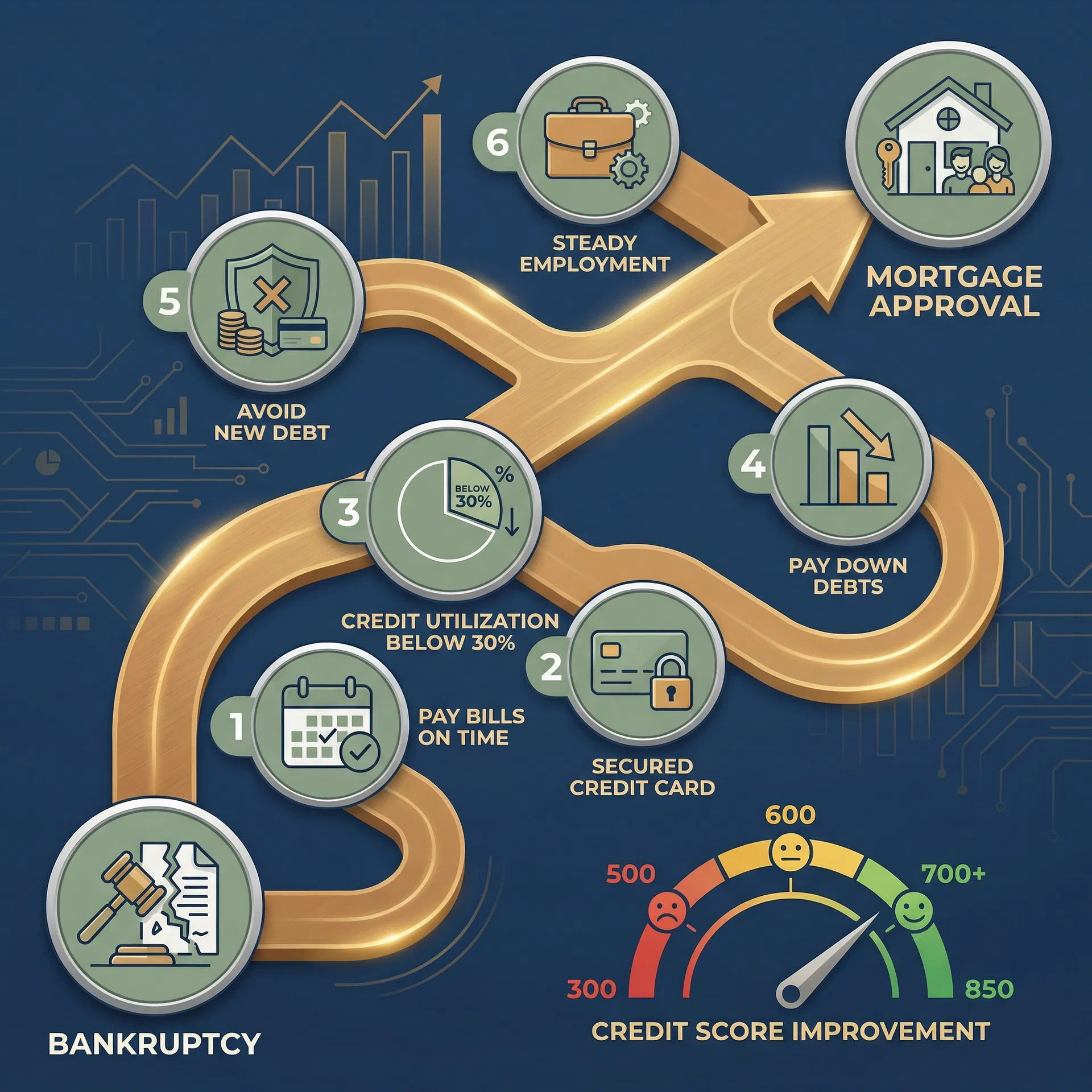

Rebuilding Your Credit After Bankruptcy

While waiting out the required seasoning period, the most productive thing you can do is actively rebuild your credit. With focused effort, most people can improve their credit score by 100-150 points within 18-24 months after bankruptcy discharge.

Six Essential Credit Rebuilding Steps

Pay All Bills On Time

Payment history accounts for thirty-five percent of your credit score. Set up automatic payments for all bills to ensure you never miss a due date. Even a single late payment can significantly damage your rebuilding efforts.

Get a Secured Credit Card

Secured credit cards require a cash deposit that becomes your credit limit. Use the card for small purchases and pay the balance in full each month. This demonstrates responsible credit use and helps rebuild your credit history.

Keep Credit Utilization Below 30%

Credit utilization—the percentage of available credit you're using—significantly impacts your score. Keep balances below thirty percent of your credit limits. Even better, aim for under ten percent for optimal credit score improvement.

Pay Down Existing Debts

Focus on reducing any remaining debts not discharged in bankruptcy. Lower debt-to-income ratios improve both your credit score and mortgage qualification prospects. Consider the debt avalanche or snowball method to stay motivated.

Avoid Accumulating New Debt

Resist the temptation to take on new debt during your credit rebuilding phase. New credit inquiries and accounts can temporarily lower your score. Focus on managing existing obligations responsibly before adding new ones.

Maintain Steady Employment

Lenders want to see stable income and employment history. Avoid job changes during your mortgage application process if possible. Two years of consistent employment in the same field significantly strengthens your application.

How to Apply for a Mortgage After Bankruptcy

Once you've completed the required waiting period and rebuilt your credit, you're ready to begin the mortgage application process. Following these steps increases your chances of approval and helps ensure a smooth transaction.

Step 1: Find Lenders Experienced with Post-Bankruptcy Loans

Not all lenders have equal experience with post-bankruptcy mortgages. Seek out lenders who specialize in or have extensive experience with bankruptcy situations. These lenders understand the nuances of bankruptcy lending guidelines and can guide you through potential challenges. They're also more likely to recognize extenuating circumstances and work with you to find solutions.

Step 2: Gather Your Documentation

Prepare your financial documentation before applying to speed up the approval process. You'll typically need:

- Complete bankruptcy petition and all related court documents

- Discharge papers (or dismissal papers if applicable)

- Two years of federal income tax returns

- Recent pay stubs covering the last thirty days

- Two months of bank statements for all accounts

- Letter of explanation detailing bankruptcy circumstances

- Documentation of extenuating circumstances (if applicable)

Step 3: Write a Compelling Letter of Explanation

A letter of explanation is your opportunity to tell your story and explain the circumstances that led to bankruptcy. This document can significantly influence a lender's decision, especially if you had extenuating circumstances. Your letter should:

- Clearly explain what caused the bankruptcy (medical emergency, job loss, divorce, etc.)

- Demonstrate that the circumstances were beyond your control

- Show what has changed since the bankruptcy to prevent recurrence

- Highlight positive financial behaviors since discharge

- Remain factual and professional without making excuses

Step 4: Get Mortgage Preapproval

Mortgage preapproval is crucial for several reasons. First, it tells you exactly how much you can afford, helping you focus your home search appropriately. Second, it demonstrates to sellers and real estate agents that you're a serious, qualified buyer—especially important given your bankruptcy history. Finally, preapproval identifies any potential issues early, giving you time to address them before finding your dream home.

Step 5: Continue Through the Mortgage Process

After preapproval and offer acceptance, stay in close contact with your lender throughout underwriting. Respond promptly to any documentation requests. Avoid making major financial changes like switching jobs, opening new credit accounts, or making large purchases. These changes can derail your approval even at the final stages.

Challenges You May Face

Understanding potential challenges helps you prepare appropriate responses and set realistic expectations. While bankruptcy doesn't permanently prevent homeownership, you may encounter some obstacles:

Higher Interest Rates

Lenders may charge higher interest rates to offset the perceived risk of lending to someone with a bankruptcy history. Even a half-point difference in rate can significantly impact your monthly payment and total interest paid over the life of the loan.

Larger Down Payment Requirements

Some lenders may require larger down payments from borrowers with bankruptcy history. While FHA and VA loans maintain standard down payment requirements, conventional lenders might ask for ten to twenty percent down instead of the typical three to five percent.

Stricter Underwriting Scrutiny

Expect more detailed review of your finances during underwriting. Lenders will carefully examine your income stability, debt-to-income ratio, and post-bankruptcy financial behavior. Be prepared to provide additional documentation and explanations.

Investor Overlays

Individual lenders may impose additional requirements beyond government program minimums. These "overlays" can include higher credit scores, larger down payments, or longer waiting periods. Shop multiple lenders to find the most favorable terms.

New Jersey-Specific Considerations

Buying a home in New Jersey after bankruptcy presents unique considerations beyond general mortgage requirements. Understanding these local factors helps you plan more effectively.

Property Taxes

New Jersey has some of the highest property taxes in the nation, with average annual bills exceeding eight thousand dollars. Lenders include property taxes in your debt-to-income ratio calculations, which can affect how much house you can afford. Factor these costs into your budget from the beginning.

Competitive Market

New Jersey's housing market remains competitive, especially in desirable areas near New York City and Philadelphia. Having a strong preapproval letter and being ready to move quickly on properties is essential. Work with a real estate agent experienced in helping buyers with credit challenges.

Local Assistance Programs

New Jersey offers several homebuyer assistance programs that can help with down payments and closing costs. The New Jersey Housing and Mortgage Finance Agency (NJHMFA) provides programs specifically for first-time buyers and those with credit challenges. These programs can make homeownership more accessible after bankruptcy.

Frequently Asked Questions

How long does it take to rebuild credit after bankruptcy?

With active credit rebuilding efforts including timely payments, secured credit cards, and low credit utilization, most people can improve their credit score by one hundred to one hundred fifty points within eighteen to twenty-four months. Those who don't actively work on credit repair may find it takes significantly longer.

Is it difficult to buy a house after bankruptcy?

While it presents additional challenges, buying a house after bankruptcy is definitely achievable. The key is understanding requirements, waiting out the necessary seasoning period, rebuilding your credit strategically, and working with experienced lenders who understand post-bankruptcy lending.

Can I qualify with a co-signer?

Yes, having a co-signer with strong credit and income can help you qualify for a mortgage after bankruptcy. The co-signer becomes equally responsible for the loan, so this typically works best with family members or close friends who understand the commitment.

Will I always pay a higher interest rate?

Not necessarily. While you may face higher rates initially after bankruptcy, as time passes and your credit improves, you can refinance to better terms. Many borrowers successfully refinance to lower rates within a few years of their initial post-bankruptcy purchase.

Should I wait longer than the minimum required period?

While you can apply as soon as you meet minimum waiting periods, waiting an additional six to twelve months often results in better terms. This extra time allows for more credit rebuilding, larger down payment savings, and potentially lower interest rates.

The Bottom Line: Homeownership After Bankruptcy Is Possible

Bankruptcy doesn't have to mean the end of your homeownership dreams. With patience, strategic planning, and focused credit rebuilding, you can successfully purchase a home in New Jersey after bankruptcy. The key is understanding the requirements for different loan programs, using your waiting period productively to rebuild credit, and working with experienced professionals who understand post-bankruptcy lending.

Start by determining which loan program best fits your situation based on the waiting periods and requirements outlined above. Use that waiting time to rebuild your credit score, save for a down payment, and gather necessary documentation. When you're ready to begin the mortgage process, seek out lenders experienced with bankruptcy situations who can guide you through potential challenges.

Remember that thousands of people successfully buy homes after bankruptcy every year. With the right approach and professional guidance, you can join them in achieving homeownership despite past financial setbacks.

Ready to Explore Your Options?

If you've experienced bankruptcy and are ready to start your journey toward homeownership in New Jersey, I can help. As a mortgage professional experienced with post-bankruptcy lending, I understand the unique challenges you face and can guide you through the process.

Disclaimer: This article provides general information about buying a home after bankruptcy and should not be considered legal or financial advice. Bankruptcy laws, mortgage requirements, and lending guidelines can change. Consult with qualified legal and financial professionals regarding your specific situation.

Related Articles

The Perks of Home Buying in the Winter Season

Discover the surprising advantages of buying a home during winter in New Jersey. Less competition, motivated sellers, and better deals await.

Buying a House Under $200K in New Jersey

Comprehensive guide to finding and financing affordable homes under $200,000 in Monmouth & Middlesex Counties.

How to Remove PMI Early: 5 Proven Strategies

Stop paying hundreds per month in Private Mortgage Insurance. Learn five proven strategies to eliminate PMI early and save thousands.