Capital Gains Tax on Home Sales: Complete Guide for New Jersey Sellers

Comprehensive guide to understanding and minimizing capital gains tax when selling your home in New Jersey. Learn about the $250K/$500K exclusion, cost basis adjustments, and tax-saving strategies that can save you thousands.

Selling your home represents one of the largest financial transactions most people will ever make. While the prospect of receiving a substantial check at closing is exciting, many New Jersey homeowners are surprised to learn they may owe capital gains tax on their profit. Understanding how this tax works and the strategies available to minimize or eliminate it can save you tens of thousands of dollars when you sell.

The good news is that federal tax law provides generous exclusions specifically designed to protect homeowners from excessive taxation on their primary residence. Combined with proper planning and documentation of home improvements, most New Jersey sellers can significantly reduce or completely eliminate capital gains tax liability. This comprehensive guide explains everything you need to know about capital gains tax on home sales and how to keep more of your hard-earned profit.

Understanding Capital Gains Tax Basics

Capital gains tax is a federal tax imposed on the profit you earn when selling an asset that has increased in value. For real estate, this means you pay tax on the difference between what you originally paid for your home and what you sell it for. The critical concept to understand is that capital gains tax applies only to your profit, not the entire sale price of your home.

The calculation starts with your cost basis, which is typically the purchase price you paid for the home. When you sell, you subtract this cost basis from the sale price to determine your capital gain. For example, if you purchased your New Jersey home for $400,000 and sell it for $600,000, your capital gain is $200,000. This $200,000 profit is what may be subject to capital gains tax, depending on various factors including how long you owned the property and whether you qualify for the primary residence exclusion.

Basic Capital Gains Calculation

Sale Price: $600,000

Original Purchase Price (Cost Basis): - $400,000

Capital Gain (Taxable Profit): $200,000

Short-Term vs. Long-Term Capital Gains

The federal government distinguishes between short-term and long-term capital gains based on how long you owned the property before selling. This distinction matters enormously because the tax rates differ dramatically, with long-term gains receiving significantly more favorable treatment.

Short-term capital gains apply when you sell a property you've owned for one year or less. These gains are taxed as ordinary income at your regular income tax rate, which can range from 10% to 37% depending on your total income. If you sell your New Jersey home after owning it for less than a year, you'll face these higher rates on your entire profit.

Long-term capital gains apply when you sell property owned for more than one year. These gains benefit from preferential tax rates of 0%, 15%, or 20%, depending on your income level. For most middle and upper-middle-class homeowners, the 15% rate applies, representing substantial savings compared to ordinary income tax rates that could be 22%, 24%, 32%, or higher.

| Tax Rate | Single Filer Income | Married Filing Jointly |

|---|---|---|

| 0% | $0 - $48,350 | $0 - $96,700 |

| 15% | $48,351 - $533,400 | $96,701 - $600,050 |

| 20% | $533,401+ | $600,051+ |

2025 Long-Term Capital Gains Tax Rates

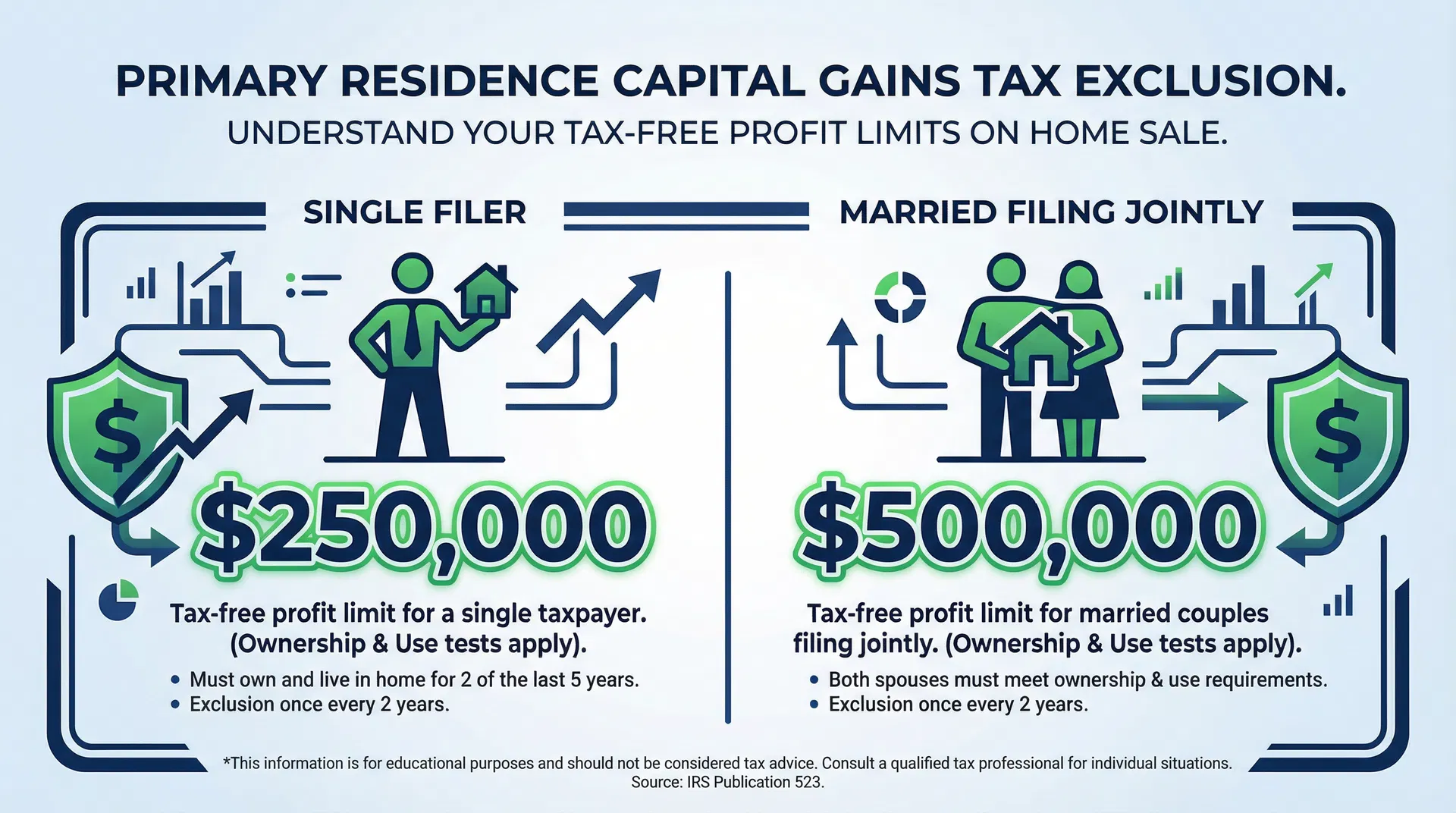

The Primary Residence Exclusion: Your Biggest Tax Break

The primary residence exclusion represents the most powerful tax-saving tool available to homeowners selling their main home. This provision allows you to exclude up to $250,000 in capital gains from taxation if you're single, or up to $500,000 if you're married filing jointly. For many New Jersey homeowners, this exclusion completely eliminates capital gains tax liability on their home sale.

Consider a married couple who purchased their New Jersey home for $400,000 and sell it fifteen years later for $850,000. Their capital gain is $450,000. Without any exclusion, they would owe significant taxes on this profit. However, with the $500,000 primary residence exclusion, their entire $450,000 gain is tax-free. They owe zero capital gains tax on the sale.

Real-World Exclusion Example

Purchase Price: $400,000

Sale Price: $850,000

Capital Gain: $450,000

Primary Residence Exclusion (Married): -$500,000

Taxable Gain: $0 (Exclusion covers entire profit)

Qualifying for the Primary Residence Exclusion

To claim the primary residence exclusion, you must satisfy three specific requirements established by the IRS. These rules ensure the exclusion benefits people selling their actual homes rather than investment properties or vacation homes.

First, the ownership test requires that you owned the home for at least two years out of the five years immediately preceding the sale. These two years don't need to be consecutive. Second, the use test requires that you lived in the home as your primary residence for at least two of those same five years. Again, these don't need to be consecutive years. Third, you cannot have claimed the exclusion on another home sale within the two years before this sale.

These requirements provide flexibility for homeowners who may have temporarily rented out their property or lived elsewhere for work. As long as you meet the two-out-of-five-years threshold for both ownership and use, you qualify for the exclusion. Special exceptions exist for military personnel, foreign service members, and certain other circumstances that may require you to sell before meeting the standard requirements.

Primary Residence Exclusion Requirements

✓ Ownership Test

You must have owned the home for at least 2 of the past 5 years before the sale

✓ Use Test

You must have lived in the home as your primary residence for at least 2 of the past 5 years

✓ Frequency Test

You haven't claimed the exclusion on another home sale in the past 2 years

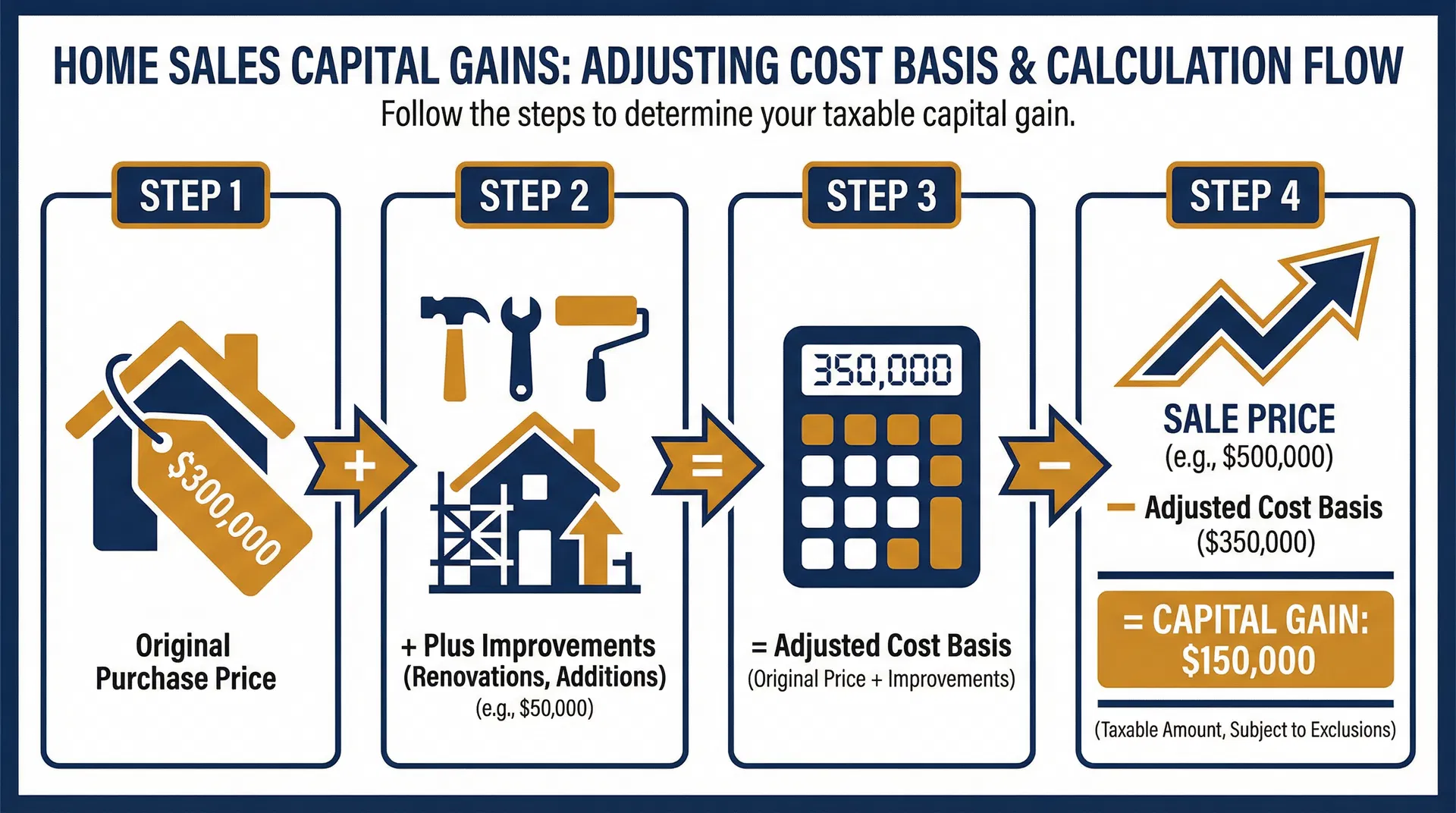

Adjusting Your Cost Basis with Capital Improvements

One of the most overlooked strategies for reducing capital gains tax involves adjusting your cost basis by adding the cost of capital improvements made during your ownership. Many homeowners fail to track these expenses and consequently pay more tax than necessary when they sell. Understanding what qualifies as a capital improvement and maintaining proper documentation can save thousands of dollars in taxes.

Capital improvements are expenditures that add value to your home, prolong its useful life, or adapt it to new uses. These differ from routine maintenance and repairs, which simply keep your home in good working condition. Adding a new room, finishing a basement, installing a new roof, upgrading your kitchen, adding a deck or patio, installing central air conditioning, or replacing windows with energy-efficient models all qualify as capital improvements.

When you make capital improvements, you can add those costs to your original purchase price to create an adjusted cost basis. This higher cost basis reduces your taxable profit when you sell. For example, if you bought your home for $400,000 and spent $75,000 finishing the basement and upgrading the kitchen, your adjusted cost basis becomes $475,000. If you sell for $600,000, your taxable gain is only $125,000 instead of $200,000, saving you significant tax dollars.

| Capital Improvements (Add to Basis) | Repairs & Maintenance (Don't Add) |

|---|---|

| Adding a room or garage | Painting interior walls |

| Finishing basement or attic | Fixing leaky faucets |

| New roof or siding | Replacing broken windows |

| Kitchen or bathroom remodel | Routine HVAC maintenance |

| New HVAC system | Lawn care and landscaping |

| Deck, patio, or fence | Repairing gutters |

| Energy-efficient windows | Cleaning carpets |

Special Considerations for Investment Properties

The rules for capital gains tax become more complex when selling investment properties or second homes. These properties do not qualify for the primary residence exclusion, meaning you'll pay capital gains tax on your entire profit after adjusting for improvements and selling costs. Additionally, if you've been depreciating a rental property on your tax returns, you'll face depreciation recapture, which can add to your tax liability.

Depreciation recapture occurs because the IRS requires you to "pay back" the tax benefits you received from depreciation deductions over the years you rented the property. The recaptured depreciation is taxed at a maximum rate of 25%, which is higher than the typical long-term capital gains rates. This additional tax can significantly impact your net proceeds from selling a rental property.

For investment properties, a 1031 exchange offers a strategy to defer capital gains taxes by reinvesting proceeds into another similar investment property. This advanced tax strategy requires strict adherence to IRS rules, including identifying replacement property within 45 days and closing within 180 days. While a 1031 exchange doesn't eliminate taxes permanently, it allows you to defer them while building wealth through real estate investing.

Proven Strategies to Minimize Capital Gains Tax

Strategic planning before selling your home can dramatically reduce or eliminate capital gains tax liability. These proven strategies work best when implemented well in advance of your sale, giving you time to meet requirements and organize documentation.

Strategy 1: Maximize the Primary Residence Exclusion

Ensure you meet both the ownership and use tests by living in your home as your primary residence for at least two of the five years before selling. If you're close to the two-year mark, waiting a few extra months to sell could save you tens of thousands in taxes by qualifying for the exclusion. For married couples, the $500,000 exclusion provides enormous tax savings on highly appreciated properties.

Strategy 2: Document All Capital Improvements

Create a comprehensive file containing receipts, invoices, contracts, and payment records for every capital improvement you make to your home. This documentation proves your adjusted cost basis and reduces your taxable gain. Even improvements made years ago can be included, so gather records going back to your purchase date. Photographs of before-and-after conditions provide additional supporting evidence.

Strategy 3: Time Your Sale Strategically

If possible, time your home sale for a year when your income is lower, as capital gains tax rates are based on your total income. Selling in a year when you're between jobs, semi-retired, or have lower income from other sources can move you into a lower tax bracket, reducing your capital gains rate from 15% to 0% or from 20% to 15%.

Strategy 4: Own for More Than One Year

Always hold your property for at least one year and one day to qualify for long-term capital gains rates rather than short-term rates. The difference between paying your ordinary income tax rate (potentially 32% or 37%) versus the long-term rate (typically 15%) represents enormous savings on large gains.

Strategy 5: Include Selling Costs in Your Calculation

Selling costs including real estate agent commissions, attorney fees, title insurance, transfer taxes, and other closing costs can be subtracted from your sale proceeds, effectively reducing your taxable gain. In New Jersey, where real estate commissions and closing costs can total 7-8% of the sale price, these deductions provide meaningful tax savings.

New Jersey-Specific Considerations

While capital gains tax is primarily a federal concern, New Jersey homeowners should be aware of state-level considerations. New Jersey does not impose a separate state capital gains tax on real estate sales; instead, capital gains are taxed as ordinary income under the state income tax system. However, New Jersey's relatively high property values mean the federal primary residence exclusion becomes especially valuable for Garden State homeowners.

In desirable New Jersey markets like Bergen County, Morris County, Monmouth County, and Princeton, homes frequently appreciate well beyond the exclusion limits, particularly for long-term owners. A couple who purchased a home in Montclair or Summit twenty years ago for $400,000 might sell today for $1.2 million or more. Even with the $500,000 exclusion, they could face substantial capital gains tax on the remaining profit, making cost basis adjustments through documented improvements critically important.

When to Consult a Tax Professional

While many straightforward home sales can be handled without specialized tax advice, certain situations warrant consultation with a qualified tax professional or CPA who specializes in real estate transactions. Complex scenarios involving investment properties, 1031 exchanges, depreciation recapture, partial exclusions, or gains exceeding the exclusion limits require expert guidance to minimize tax liability and ensure compliance.

If you're selling a high-value property where gains will exceed the $250,000 or $500,000 exclusion, a tax professional can help you explore additional strategies to reduce your tax burden. Similarly, if you've converted a primary residence to a rental property or vice versa, the rules become more nuanced and professional advice ensures you claim all available benefits while avoiding costly mistakes.

Final Thoughts: Plan Ahead to Maximize Your Proceeds

Understanding capital gains tax and the strategies available to minimize it represents an essential component of successful home selling. For most New Jersey homeowners selling their primary residence, the generous federal exclusion combined with proper documentation of improvements will eliminate or dramatically reduce capital gains tax liability. However, this favorable outcome requires planning, documentation, and awareness of the rules.

Start preparing for your eventual sale today by creating a comprehensive file of all capital improvements, maintaining receipts and records, and understanding whether you meet the requirements for the primary residence exclusion. When the time comes to sell, you'll have the documentation and knowledge necessary to minimize your tax burden and keep more of your hard-earned profit.

If you're considering selling your New Jersey home and have questions about how capital gains tax might affect your proceeds, or if you're planning a purchase and want to understand the long-term tax implications, professional guidance can help you make informed decisions that align with your financial goals.

Questions About Selling Your Home?

Whether you're planning to sell soon or thinking ahead, I can help you understand how capital gains tax might affect your situation and connect you with qualified tax professionals when needed.

Disclaimer: This article provides general information about capital gains tax for educational purposes. Tax laws are complex and subject to change. Consult with a qualified tax professional or CPA for advice specific to your situation. Matthew Victoria is a mortgage professional, not a tax advisor.

Related Articles

How to Get a Home Renovation Loan in New Jersey: Complete 2026 Guide

Comprehensive guide to financing your home improvements in New Jersey. Learn about FHA 203(k), HomeStyle, VA renovation loans, and qualification requirements.

Strategic Guide to Timing Your Home Sale

Learn how to balance tax implications, market conditions, seasonal factors, and personal circumstances for optimal home selling timing.

The Perks of Home Buying in the Winter Season

Discover the surprising advantages of buying a home during winter in New Jersey. Less competition, motivated sellers, and better deals await.