Buying a Home After Foreclosure: Your Complete Recovery Guide for New Jersey

Foreclosure doesn't mean the end of homeownership. Discover the waiting periods, loan options, credit rebuilding strategies, and proven steps to buy a home again in New Jersey after foreclosure.

Experiencing foreclosure is one of the most challenging financial setbacks a homeowner can face. The emotional toll, credit damage, and uncertainty about the future can feel overwhelming. However, foreclosure is not a permanent barrier to homeownership. Thousands of New Jersey residents successfully rebuild their financial lives and purchase homes again after foreclosure every year. Understanding the waiting periods, loan options, credit rebuilding strategies, and systematic steps to recovery can transform what feels like an insurmountable obstacle into a manageable path forward.

The key to successful recovery lies in understanding that different mortgage programs have different waiting periods and requirements after foreclosure. While conventional loans may require seven years of waiting, government-backed programs like FHA, VA, and USDA offer much shorter timelines—sometimes as little as two years. Additionally, demonstrating extenuating circumstances that led to the foreclosure can further reduce these waiting periods. This guide provides New Jersey homebuyers with a comprehensive roadmap to navigate foreclosure recovery, rebuild credit, and achieve homeownership again.

Understanding Foreclosure and Its Impact

Foreclosure occurs when a homeowner fails to make mortgage payments, and the lender takes legal action to repossess and sell the property to recover the outstanding loan balance. In New Jersey, foreclosure is a judicial process, meaning it goes through the court system and typically takes 12 to 18 months from the first missed payment to the final sale. This extended timeline provides opportunities for homeowners to explore alternatives like loan modifications, short sales, or deed-in-lieu arrangements, which can have less severe long-term consequences than a completed foreclosure.

The impact of foreclosure on your financial life is significant but not permanent. Your credit score will drop substantially—typically 200 to 400 points depending on your starting score and overall credit profile. The foreclosure remains on your credit report for seven years from the date of the first missed payment that led to the foreclosure. However, the impact diminishes over time, especially as you rebuild positive credit history. Beyond credit scores, foreclosure affects your ability to qualify for new mortgages, rental housing, insurance rates, and sometimes even employment opportunities in financial sectors.

Types of Foreclosure in New Jersey

New Jersey uses judicial foreclosure, which requires lenders to file a lawsuit and obtain a court judgment before selling the property. This process provides homeowners with multiple opportunities to respond, negotiate, or cure the default. The typical timeline includes a notice of intent to foreclose, a complaint filing, a court hearing, a judgment of foreclosure, and finally a sheriff's sale. Understanding this timeline is crucial because the date of the foreclosure completion (typically the sheriff's sale date) determines when your waiting period begins for future mortgage eligibility.

Some homeowners pursue alternatives to completed foreclosure that can reduce long-term consequences. A short sale, where the lender agrees to accept less than the full loan balance, typically results in a shorter waiting period (two to four years depending on the loan program). A deed-in-lieu of foreclosure, where the homeowner voluntarily transfers the property to the lender, may also result in reduced waiting periods. However, these alternatives still negatively impact credit and require waiting periods before qualifying for a new mortgage.

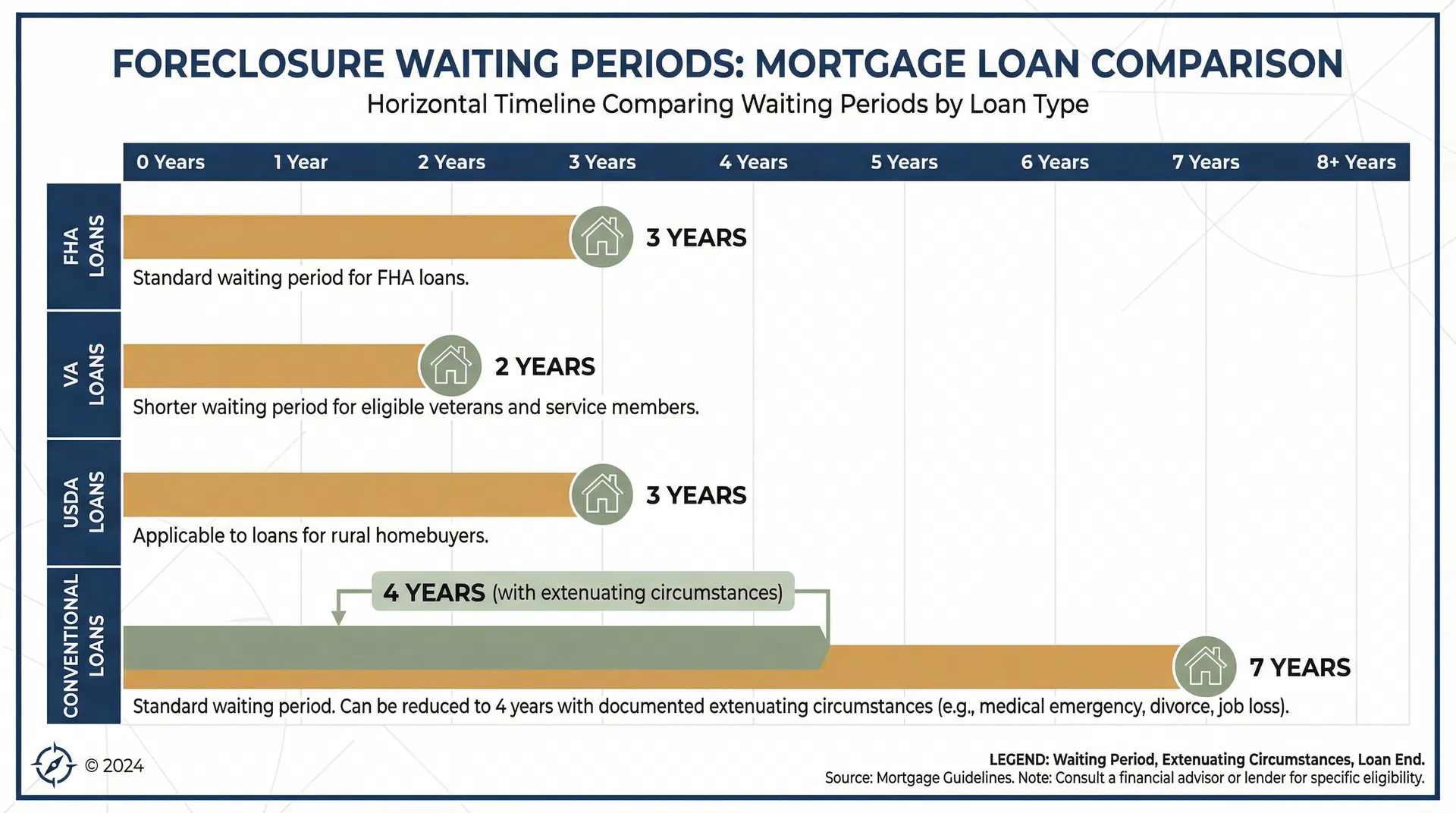

Mortgage Waiting Periods After Foreclosure

Different mortgage programs have vastly different waiting periods after foreclosure. Understanding these timelines helps you set realistic expectations and plan your recovery strategy. The waiting period begins from the date the foreclosure is completed (typically the sale date), not from the date of the first missed payment. Additionally, demonstrating extenuating circumstances—such as job loss, medical emergency, divorce, or death of a primary wage earner—can significantly reduce these waiting periods across all loan programs.

FHA Loans: 3-Year Standard Waiting Period

FHA loans offer one of the shortest standard waiting periods at three years from the foreclosure completion date. However, this timeline can be reduced to just one year if you can document extenuating circumstances that caused the foreclosure and demonstrate that you've re-established good credit since then. Extenuating circumstances must be beyond your control, such as a serious illness, death of a primary wage earner, or divorce. Job loss alone typically doesn't qualify unless it resulted from a company closure or mass layoff.

To qualify for an FHA loan after foreclosure, you'll need a minimum credit score of 580 for 3.5% down payment or 500-579 for 10% down payment. You must demonstrate 12 months of on-time payments on all credit accounts since the foreclosure, maintain a debt-to-income ratio below 43% (sometimes up to 50% with compensating factors), and provide documentation explaining the foreclosure circumstances. FHA loans are particularly attractive for New Jersey buyers because they allow lower credit scores and down payments compared to conventional loans.

VA Loans: 2-Year Waiting Period for Veterans

VA loans offer the shortest waiting period at just two years from foreclosure completion for eligible veterans, active-duty service members, and qualifying surviving spouses. This benefit recognizes the service and sacrifice of military members and provides them with an accelerated path back to homeownership. Like FHA loans, VA loans don't have a minimum credit score requirement set by the VA itself, though individual lenders typically require scores of 580 to 620 or higher.

One important consideration for VA loans after foreclosure is that if your previous foreclosure involved a VA loan, you may have reduced entitlement until the VA loss is repaid. This doesn't necessarily prevent you from getting another VA loan, but it may affect the loan amount you can obtain without a down payment. Additionally, you'll need to demonstrate satisfactory credit re-establishment, typically meaning 12 months of on-time payments on all accounts since the foreclosure. The two-year waiting period can potentially be reduced with documented extenuating circumstances, though this is evaluated on a case-by-case basis.

USDA Loans: 3-Year Waiting Period for Rural Properties

USDA loans, which finance homes in eligible rural and suburban areas, require a three-year waiting period from foreclosure completion. In New Jersey, many areas in counties like Sussex, Warren, Salem, and parts of Hunterdon, Burlington, and Ocean counties qualify for USDA financing. These loans offer 100% financing (no down payment required) and competitive interest rates, making them attractive options for buyers who meet the income and property location requirements.

To qualify for a USDA loan after foreclosure, you'll need a minimum credit score of 640 (though some lenders may accept 620 with compensating factors), demonstrate 12 months of satisfactory credit since the foreclosure, meet income limits for the area (typically 115% of median household income), and purchase a property in an eligible rural area. The three-year waiting period can potentially be reduced to one year with documented extenuating circumstances, though USDA guidelines are strict about what qualifies as extenuating.

Conventional Loans: 7-Year Standard, 4-Year with Extenuating Circumstances

Conventional loans backed by Fannie Mae and Freddie Mac have the longest waiting periods after foreclosure. The standard timeline is seven years from the foreclosure completion date. However, if you can document extenuating circumstances that caused the foreclosure and demonstrate that you've fully recovered financially, the waiting period can be reduced to four years. This is still significantly longer than government-backed loan programs, making FHA, VA, or USDA loans more attractive options for most foreclosure recovery situations.

For the four-year reduced waiting period, you must provide documentation of extenuating circumstances (job loss due to company closure, serious illness with medical bills, divorce, death of wage earner), demonstrate that the circumstances were beyond your control and are unlikely to recur, show that you've re-established good credit with 12 months of on-time payments, and maintain a debt-to-income ratio within guidelines (typically 43% to 45%). Conventional loans typically require higher credit scores (620 minimum, 680+ for best rates) and larger down payments (5% to 20%) compared to government-backed programs.

Credit Rebuilding Strategies After Foreclosure

Rebuilding your credit after foreclosure is essential for qualifying for a new mortgage and obtaining favorable interest rates. While the foreclosure itself will remain on your credit report for seven years, its impact diminishes significantly over time, especially as you establish new positive credit history. The key is to demonstrate consistent, responsible credit management through strategic actions that show lenders you've recovered from the financial setback and are now a reliable borrower.

Establish New Positive Payment History

The single most important factor in credit rebuilding is establishing a consistent pattern of on-time payments. Payment history accounts for 35% of your credit score, making it the most heavily weighted factor. After foreclosure, you need to demonstrate at least 12 months of perfect payment history on all credit accounts before most lenders will consider you for a new mortgage. This includes credit cards, auto loans, student loans, personal loans, and even utility bills if they're reported to credit bureaus.

If you don't currently have any active credit accounts, you'll need to establish new credit carefully. Start with a secured credit card, where you deposit money as collateral and receive a credit limit equal to your deposit. Use the card for small purchases each month and pay the full balance on time. After six months of responsible use, many secured cards convert to unsecured cards and return your deposit. You can also consider becoming an authorized user on a family member's account with good payment history, though not all lenders give full credit for authorized user status.

Maintain Low Credit Utilization

Credit utilization—the percentage of available credit you're using—accounts for 30% of your credit score. After foreclosure, it's crucial to keep your credit utilization below 30% on each card and ideally below 10% overall for optimal credit score recovery. This means if you have a credit card with a $1,000 limit, you should keep the balance below $300 at all times, and preferably below $100. High utilization signals financial stress to lenders, even if you're making on-time payments.

A common strategy is to make multiple payments throughout the month to keep your reported balance low. Credit card companies typically report your balance to credit bureaus on your statement closing date, not your payment due date. By making payments before your statement closes, you can keep your reported utilization low even if you use the card regularly. For example, if you charge $500 to your card during the month but make a $400 payment before the statement closes, only $100 will be reported as your balance.

Diversify Your Credit Mix

Credit mix accounts for 10% of your credit score and refers to having different types of credit accounts—revolving credit (credit cards) and installment loans (auto loans, personal loans, student loans). After foreclosure, having a diverse mix of credit that you're managing responsibly demonstrates to lenders that you can handle various types of financial obligations. However, don't take on debt you don't need just to improve your credit mix; only pursue credit that makes financial sense for your situation.

If you need to finance a vehicle, an auto loan can help rebuild credit while serving a practical purpose. Make sure to shop for the best rates and terms, and avoid subprime lenders with predatory rates that can trap you in a cycle of debt. Credit builder loans, offered by some credit unions and online lenders, are specifically designed to help rebuild credit. With these loans, the borrowed amount is held in a savings account while you make monthly payments; once the loan is paid off, you receive the funds. This creates positive payment history without requiring you to take on additional debt.

Monitor Your Credit Reports Regularly

After foreclosure, it's essential to monitor your credit reports from all three major bureaus (Equifax, Experian, TransUnion) to ensure accuracy and track your progress. You're entitled to one free credit report from each bureau every 12 months through AnnualCreditReport.com. Review each report carefully for errors, such as accounts that don't belong to you, incorrect payment statuses, or duplicate entries. Dispute any inaccuracies immediately, as errors can further damage your already compromised credit.

Consider using a credit monitoring service that provides regular updates on your credit score and alerts you to changes in your credit report. Many credit card companies and banks offer free credit score tracking as a benefit to customers. Monitoring your credit helps you identify potential identity theft quickly, track your recovery progress, understand which factors are most affecting your score, and know when you've reached credit score thresholds that qualify you for better loan terms.

Saving for Your Down Payment and Closing Costs

While rebuilding credit, simultaneously focus on saving for your down payment and closing costs. The amount you'll need depends on the loan program you choose. FHA loans require as little as 3.5% down (though 10% if your credit score is below 580), VA and USDA loans offer 100% financing with no down payment required, and conventional loans typically require 5% to 20% down. In New Jersey, where median home prices range from $300,000 to $500,000 depending on the area, this translates to $10,500 to $100,000 in down payment funds.

Beyond the down payment, budget for closing costs, which typically range from 2% to 5% of the purchase price. For a $400,000 home in New Jersey, expect $8,000 to $20,000 in closing costs, including lender fees, appraisal, title insurance, attorney fees, recording fees, and prepaid property taxes and insurance. Some loan programs allow sellers to contribute toward closing costs (up to 6% for FHA loans, unlimited for VA loans), which can significantly reduce your out-of-pocket expenses at closing.

Create a Dedicated Savings Plan

Develop a systematic savings plan with specific monthly targets. Calculate how much you need to save total (down payment plus closing costs), determine your timeline (when you'll be eligible for a mortgage based on waiting periods), and divide the total by the number of months to determine your monthly savings goal. For example, if you need $30,000 in three years, you'll need to save approximately $833 per month. Automate transfers to a dedicated savings account to ensure consistent progress.

Look for opportunities to accelerate your savings through side income, tax refunds, work bonuses, selling unused items, reducing discretionary spending, and refinancing other debts to lower monthly payments. Every extra dollar saved reduces your timeline to homeownership and may allow you to make a larger down payment, which can result in better loan terms and lower monthly payments. Consider high-yield savings accounts or short-term CDs to earn interest on your down payment savings while keeping the funds accessible.

Document Your Savings Sources

Mortgage lenders require documentation of where your down payment and closing costs funds come from, typically requesting two months of bank statements. After foreclosure, lenders scrutinize your finances more carefully, so it's essential to maintain clean, well-documented savings. Avoid large cash deposits that can't be explained, as lenders may not count these funds toward your down payment. If you receive gift funds from family members, you'll need a gift letter stating that the funds don't need to be repaid.

Keep your down payment funds in a stable account and avoid moving money between accounts frequently in the months before applying for a mortgage. Each transfer creates additional documentation requirements and can complicate your loan application. If you must move funds, keep clear records of the transfers and be prepared to explain them to your lender. The goal is to demonstrate financial stability and that your down payment comes from legitimate, documented sources.

Establishing Stable Housing History

After foreclosure, establishing a stable housing payment history is crucial for demonstrating to lenders that you can manage housing expenses responsibly. Whether you're renting an apartment, living with family, or in another housing situation, documenting consistent, on-time housing payments strengthens your mortgage application significantly. Lenders typically want to see at least 12 months of perfect housing payment history before approving a new mortgage after foreclosure.

If you're renting, ensure your landlord reports your payments to credit bureaus or be prepared to provide canceled checks, bank statements, or a verification of rent form from your landlord. Some rent reporting services can add your rental payment history to your credit reports for a fee, which can be valuable if your landlord doesn't report payments automatically. If you're living with family or in a situation where you're not making traditional housing payments, be prepared to explain this arrangement to lenders and demonstrate that you're saving money that would otherwise go toward housing costs.

The Mortgage Application Process After Foreclosure

When you're ready to apply for a mortgage after foreclosure, the process will be more thorough than a standard application. Lenders will scrutinize your financial recovery carefully, requiring extensive documentation of your credit rebuilding efforts, income stability, savings accumulation, and the circumstances that led to the foreclosure. Being prepared with comprehensive documentation and a clear narrative about your recovery can significantly improve your chances of approval and favorable terms.

Letter of Explanation

You'll need to write a detailed letter of explanation addressing the foreclosure. This letter should explain what circumstances led to the foreclosure (job loss, medical emergency, divorce, etc.), what you've done to recover financially since then (new employment, credit rebuilding, savings), why those circumstances are unlikely to recur, and why you're now a good credit risk. Be honest, specific, and factual. Avoid making excuses or blaming others; instead, focus on taking responsibility and demonstrating the concrete steps you've taken to ensure it won't happen again.

Support your letter with documentation such as termination letters from previous employment, medical bills or records if health issues contributed to the foreclosure, divorce decrees if marital dissolution was a factor, and evidence of new employment and stable income. The more documentation you can provide to support your explanation, the stronger your application will be. Work with your loan officer to craft a compelling narrative that addresses lender concerns while highlighting your financial recovery.

Demonstrating Financial Stability

Beyond the waiting period and credit score requirements, lenders want to see evidence of overall financial stability. This includes steady employment (typically two years in the same field, though job changes for advancement are acceptable), consistent income that adequately covers your proposed mortgage payment and other debts, substantial savings beyond just the down payment and closing costs (reserves), and a clean payment history on all accounts since the foreclosure. The stronger your overall financial profile, the more likely you are to receive approval and favorable terms.

Lenders typically want to see reserves—additional savings beyond your down payment and closing costs—equal to two to six months of mortgage payments. For a $2,500 monthly mortgage payment, this means $5,000 to $15,000 in additional savings. Reserves demonstrate that you can continue making mortgage payments even if you experience a temporary income disruption. After foreclosure, having substantial reserves can be the difference between approval and denial, as it provides lenders with confidence in your ability to weather financial challenges.

Working with the Right Lender

Not all lenders have the same appetite for working with borrowers who have experienced foreclosure. Some lenders strictly enforce minimum waiting periods and credit score requirements, while others have more flexible underwriting that considers the full context of your situation. Finding a lender experienced in credit-challenged borrowers and willing to work with your specific circumstances can significantly improve your chances of approval and may result in better terms.

Look for lenders who specialize in FHA, VA, or USDA loans if you're pursuing those programs, as they'll have more experience navigating the specific guidelines and exceptions available. Ask potential lenders about their experience with foreclosure recovery cases, their approval rates for borrowers with past foreclosures, whether they offer manual underwriting (human review rather than automated systems), and what documentation they'll need to support your application. A knowledgeable loan officer can guide you through the process, help you present your case effectively, and identify the best loan program for your situation.

New Jersey-Specific Considerations

New Jersey's high property costs, property taxes, and cost of living create unique challenges for foreclosure recovery. The median home price in New Jersey is approximately $500,000, significantly higher than the national median. Property taxes in New Jersey are the highest in the nation, averaging $9,000 to $12,000 annually in many counties. These factors mean that even with a mortgage approval, you'll need to carefully consider whether you can afford the total housing costs, including property taxes, insurance, utilities, and maintenance.

Consider targeting more affordable areas within New Jersey or neighboring Pennsylvania if you work near the border. Counties like Salem, Cumberland, and parts of Atlantic County offer lower home prices and property taxes compared to North Jersey counties. Alternatively, focus on condos or townhomes, which typically have lower purchase prices and property taxes than single-family homes. The key is to ensure that your housing costs (including all expenses) don't exceed 28% to 31% of your gross monthly income, which is the standard lender guideline for housing expense ratios.

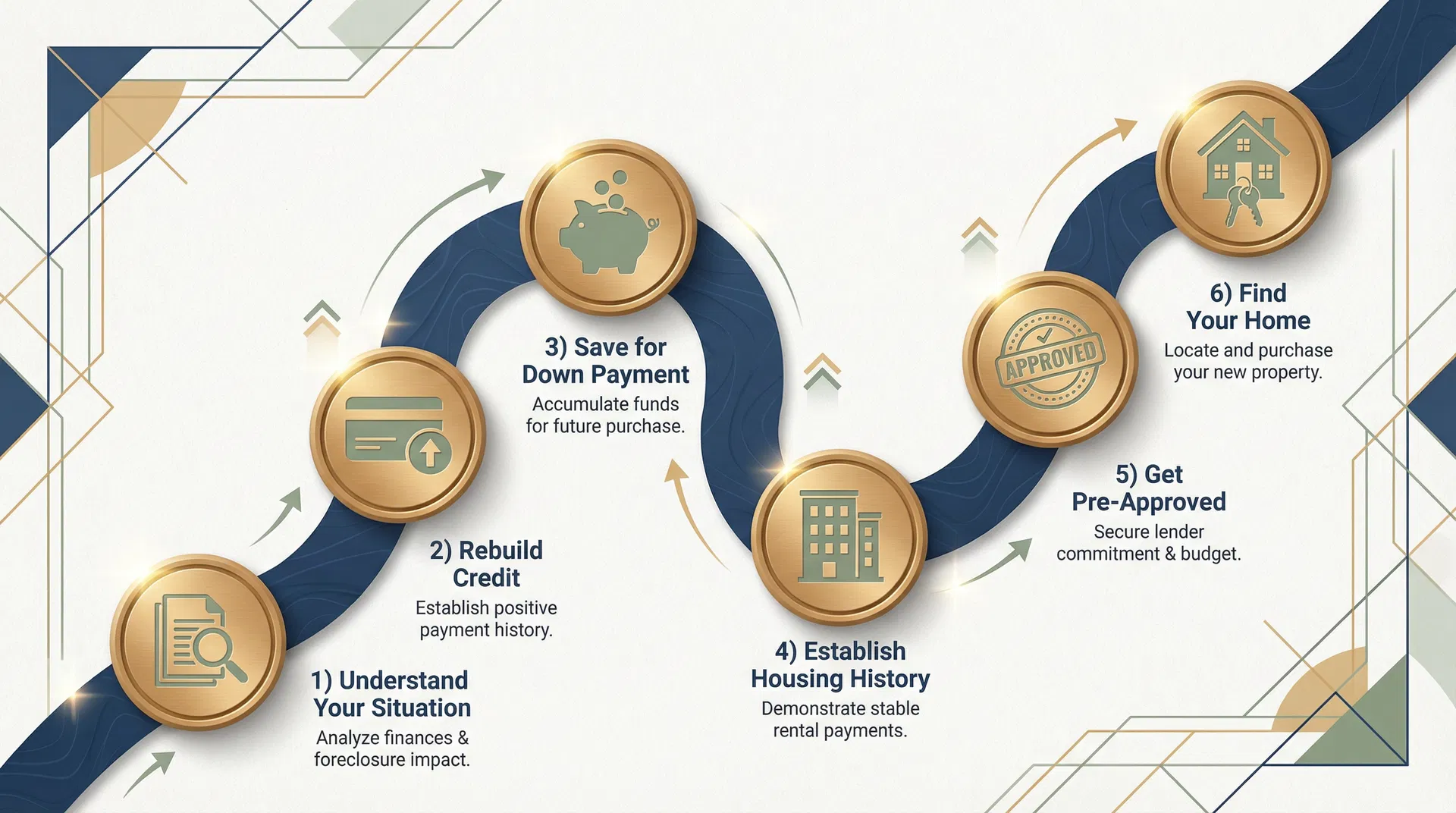

Your Action Plan for Foreclosure Recovery

6-Step Recovery Roadmap

- 1Understand Your Situation (Months 0-3)

Obtain your credit reports, determine your foreclosure completion date, identify which loan programs you'll be eligible for and when, and calculate your target credit score and savings goals.

- 2Rebuild Credit Aggressively (Months 1-24)

Establish new credit accounts (secured cards, credit builder loans), make every payment on time without exception, keep credit utilization below 30% (ideally below 10%), and monitor your credit reports monthly for errors.

- 3Save for Down Payment and Reserves (Months 1-36)

Create automated savings plan, calculate total funds needed (down payment + closing costs + reserves), keep funds in documented accounts, and avoid large cash deposits or unexplained transfers.

- 4Establish Housing Payment History (Months 12-36)

Make all housing payments on time (rent, mortgage if co-signing, etc.), document payments with canceled checks or bank statements, consider rent reporting services if landlord doesn't report, and maintain stable housing situation without frequent moves.

- 5Get Pre-Approved (Months 24-36)

Connect with experienced lender 6 months before eligibility date, gather all required documentation, prepare detailed letter of explanation, and obtain pre-approval to understand your buying power.

- 6Find Your Home and Close (Months 36+)

Work with experienced real estate agent, target homes within your pre-approved budget, be prepared for additional documentation requests, and maintain financial stability throughout the process (no new credit, job changes, or large purchases).

Frequently Asked Questions

Can I buy a house immediately after foreclosure?

No, all mortgage programs require waiting periods after foreclosure. The shortest is two years for VA loans, followed by three years for FHA and USDA loans, and seven years (or four with extenuating circumstances) for conventional loans. These waiting periods begin from the foreclosure completion date.

What credit score do I need after foreclosure?

Minimum credit score requirements vary by loan program: FHA loans require 580 for 3.5% down or 500-579 for 10% down, VA loans have no official minimum but lenders typically require 580-620, USDA loans require 640 (sometimes 620), and conventional loans require 620 minimum (680+ for best rates). Focus on rebuilding your score to at least 620-640 for the most options.

What qualifies as extenuating circumstances?

Extenuating circumstances are events beyond your control that caused the foreclosure, such as serious illness or medical emergency with substantial bills, death of a primary wage earner, divorce or legal separation, job loss due to company closure or mass layoff, or natural disaster. You must provide documentation and demonstrate that the circumstances are unlikely to recur.

Should I wait the full seven years for a conventional loan or pursue FHA/VA earlier?

For most borrowers, pursuing FHA, VA, or USDA loans with shorter waiting periods makes more financial sense than waiting seven years for a conventional loan. The sooner you can buy, the sooner you build equity and stop paying rent. You can always refinance to a conventional loan later once you've rebuilt equity and credit. The exception might be if you're very close to the seven-year mark and have excellent credit and substantial down payment saved.

Will I need a larger down payment after foreclosure?

Down payment requirements are determined by the loan program, not your foreclosure history. FHA loans require 3.5% down (10% if credit score is below 580), VA and USDA loans offer 100% financing, and conventional loans require 5% to 20% down. However, making a larger down payment can strengthen your application and may result in better terms, so save as much as you reasonably can.

Can I remove the foreclosure from my credit report early?

Foreclosures remain on your credit report for seven years from the date of the first missed payment that led to the foreclosure. You cannot remove accurate foreclosure information early unless it's being reported incorrectly. However, the impact on your credit score diminishes over time, especially as you build new positive credit history. Focus on rebuilding rather than trying to remove the foreclosure.

Take the First Step Toward Homeownership Again

Foreclosure is a significant financial setback, but it's not a permanent barrier to homeownership. With the right strategy, consistent effort, and patience, you can rebuild your credit, save for a down payment, and qualify for a mortgage again. The key is to start immediately—every month of on-time payments, every dollar saved, and every point your credit score increases brings you closer to owning a home again in New Jersey.

Remember that your timeline to homeownership depends on the loan program you choose, your ability to document extenuating circumstances, and how aggressively you rebuild your credit and savings. FHA loans with three-year waiting periods (potentially reduced to one year) and VA loans with two-year waiting periods offer the fastest paths back to homeownership for most borrowers. Focus on the factors within your control—payment history, credit utilization, savings, and financial stability—and you'll be well-positioned to achieve your homeownership goals.

Ready to Start Your Foreclosure Recovery Journey?

I specialize in helping New Jersey homebuyers navigate credit challenges and achieve homeownership after foreclosure. Let's discuss your specific situation and create a personalized plan to get you back into a home.

Disclaimer: This article provides general information about foreclosure recovery and mortgage eligibility. Individual circumstances vary, and waiting periods, credit requirements, and loan terms depend on your specific situation, the loan program, and lender guidelines. Consult with a qualified mortgage professional to discuss your specific foreclosure recovery plan and mortgage options. This content is for educational purposes only and does not constitute financial or legal advice.

Related Articles

How to Get a Home Renovation Loan in New Jersey: Complete 2026 Guide

Comprehensive guide to financing your home improvements in New Jersey. Learn about FHA 203(k), HomeStyle, VA renovation loans, and qualification requirements.

Strategic Guide to Timing Your Home Sale

Learn how to balance tax implications, market conditions, seasonal factors, and personal circumstances for optimal home selling timing.

Capital Gains Tax on Home Sales: Complete Guide

Understanding and minimizing capital gains tax when selling your home in New Jersey. Learn about the $250K/$500K exclusion and tax-saving strategies.